nashi Team

5 min read

Running a retail store in Singapore means navigating a crowded market of payment tools. Each provider makes bold claims about simplicity, savings, and service. But not every retailer needs the same solution.

The right POS system depends on what you sell, how you sell it, and your appetite for complexity. Some retailers need full inventory management and SKU tracking. Others just need a fast, affordable way to accept cards.

This guide covers the 6 best POS systems and payment solutions for retail stores in Singapore in 2026. Each is evaluated on pricing, setup costs, features, and who it's genuinely built for.

What are the best POS systems for retail stores in Singapore?

The top 6 options are nashi, HitPay, Qashier, Stripe, NETS Tap-to-Phone, and Grab Tap to Phone.

nashi is the best choice for small retailers who want hardware-free card acceptance without the complexity of a full POS. HitPay is the most established all-in-one platform, covering in-person payments, PayNow, e-commerce, and invoicing in one dashboard. Qashier is the strongest option for retailers who need a full POS with inventory management and SKU tracking.

Stripe suits tech-forward retailers running both online and in-person sales. NETS Tap-to-Phone is a solid choice for traditional brick-and-mortar stores where NETS debit card acceptance matters. Grab Tap to Phone offers competitive rates but adds 9% GST on all fees. It's most useful for merchants already serving the Grab ecosystem.

Platform | Starting Price | Best For | Key Differentiator |

|---|---|---|---|

nashi | From 1.99% + $0.30 | Small retailers, card acceptance only | Hardware-free, 1-day onboarding |

HitPay | 2.5% (min $0.20) | All-in-one payment platform | PayNow, e-commerce, invoicing |

Qashier | Free (Lite) / S$56/mo (Essential) + Transaction Fees | Full retail POS with inventory | Inventory, loyalty, multi-outlet |

Stripe | 3.4% + $0.50 | Omnichannel, tech-forward retailers | Developer ecosystem, online + in-person |

NETS Tap-to-Phone | ~$29.90/mo + up to 3.5% | Traditional brick-and-mortar | NETS debit card acceptance |

Grab Tap to Phone | 2.50% + 9% GST | GrabPay ecosystem merchants | GrabPay at 0.80% |

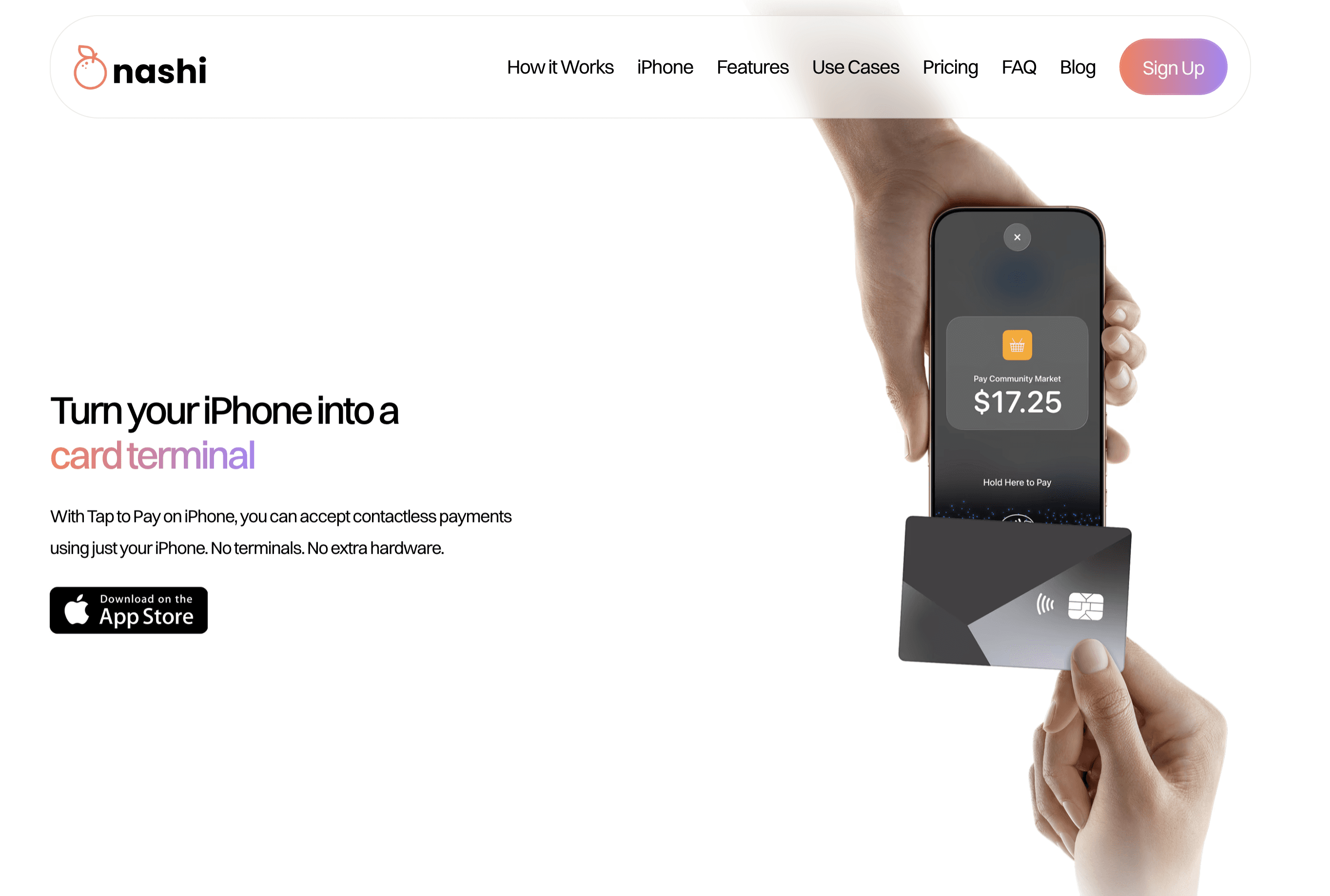

1. nashi: Best for hardware-free card acceptance

Disclosure: nashi is our own product. We've included it because we believe it genuinely belongs on this list, but you should know we're not a neutral party.

nashi is not a full POS system — it doesn't offer inventory management, SKU tracking, or e-commerce. What it does, it does extremely well. It turns any NFC-enabled Android or iPhone phone into a card terminal, with no hardware required.

For small retail businesses that primarily need to accept cards, nashi removes the usual friction. No terminal to buy, no Bluetooth to sync, no monthly fee regardless of how often you sell. Market stalls, pop-up shops, boutiques, and fragrance brands have been early adopters.

Onboarding is entirely digital and takes roughly 1 business day. You'll need your latest details which can be extracted trough CorpPass, IDs of majority shareholders, and a bank statement. Everything is done in the app.

Key features

Hardware-free — accepts card payments using only your existing NFC-enabled Android phone; no terminal or accessory required

Accepts Visa, Mastercard, and Amex — physical cards and mobile wallets supported

Digital onboarding — complete KYC entirely in the app; typically approved within 1 business day

Settlements — automatic payouts to your bank account within 2 business days

Refunds — full or partial refunds issued directly through the app

Segment-specific pricing — list pricing published on the website; nashi will discuss rates based on your industry and business maturity

Pricing

Card Type | Rate |

|---|---|

Singapore Visa / Mastercard | From 1.99% + $0.30 |

Amex | 3.3% + $0.30 |

International Visa / Mastercard | 3.3% + $0.30 |

Published list pricing: 1.99% for businesses new to cards; 2.7% for all other categories. No GST on fees, no monthly fee, no setup fee.

Pros & cons

Pros:

Available on Android and iOS

$0 setup, $0 monthly — no sunk cost before your first transaction

Fastest onboarding in the category — typically 1 business day

Accepts Amex — most competitors in Singapore do not

No GST on transaction fees, unlike Fiuu and Grab

No hardware costs — use the Android phone you already own

PCI-DSS compliant, powered by Adyen's payment infrastructure

Cons:

Not a full POS — no inventory management, SKU tracking, or e-commerce

Not competitive for F&B or low-value transactions (e.g. $5 coffees)

In-person card acceptance only, no e-commerce solution

Customers

nashi serves micro and small businesses across Singapore. Retailers, fragrance and skincare brands, pop-up vendors, makeup artist, fitness professionals and wholesalers have been among the earliest adopters. It is purpose-built for sole proprietors and small Pte Ltd companies who prefer card acceptance over full POS complexity.

2. HitPay: Best all-in-one payment platform

HitPay is the most recognised name in Singapore's small business payment space. It covers Tap to Phone, PayNow, payment links, e-commerce, invoicing, BNPL, and a website builder. It's a full platform — not just a card acceptance tool.

If your store operates online and in-person, HitPay is a natural starting point. It supports both Android and iOS, charges no setup fee or monthly fee, and doesn't add GST on transaction fees.

The trade-offs are real. Public reviews on Trustpilot and app stores describe onboarding delays and account holds without warning.

Inconsistent support is a recurring theme — not ideal for retailers racing to get started. Custom rates are only available to merchants processing over S$50,000 per month.

Key features

Full payment suite: Tap to Phone, PayNow, payment links, e-commerce, invoicing, BNPL, website builder

Available on both Android and iOS

Accepts Visa, Mastercard, and Amex

No setup fee, no monthly fee, no GST on transaction fees

Pricing

Card Type | Rate |

|---|---|

Singapore Visa / Mastercard | 2.5% (min fee S$0.20) |

Amex | 2.5% (min fee S$0.20) |

International Visa / Mastercard | 3.20% |

Pros & cons

Pros:

Most established local brand for small business payments in Singapore

Broadest feature set — covers all payment channels in one platform

No setup fee, no monthly fee, no GST on fees

Available on both Android and iOS

Accepts Amex at the same rate as Visa and Mastercard

Cons:

Feature-heavy — overwhelming for retailers who only need in-person card acceptance

Onboarding delays and account hold issues documented in public reviews

Support quality inconsistent based on Trustpilot and app store feedback

Custom rates require S$50,000+/month — most small retailers won't qualify

Not purpose-built for mobile or intermittent retail use

Customers

HitPay is widely used by Singapore e-commerce brands that also sell in-person — commonly seen at pop-ups alongside their online storefronts. It's a strong fit for retailers who want one platform to handle both channels.

3. Qashier: Best full POS with inventory management

Qashier is a full POS platform for retailers who need more than card acceptance. It combines sales, inventory, customer loyalty, and payments in one system. The flagship hardware — QashierPOS — is a smart terminal with dual touchscreens and a built-in receipt printer.

Unlike tap-to-phone solutions, Qashier is hardware-based. It goes well beyond card acceptance: inventory and SKU tracking, a loyalty programme, and multi-outlet management from one central dashboard. It also works offline, syncing transactions to the cloud when your connection returns.

Pricing has two tiers: a free Lite plan for entry-level needs and an Essential plan at S$56/month. Hardware is available through a subscription model — Qashier markets it as "as low as $1 a day." Transaction rates through QashierPay are not publicly published; contact Qashier directly.

Key features

QashierPOS hardware — smart terminal with dual touchscreens and a built-in receipt printer

Inventory management — full stock and SKU tracking across your product catalogue

QashierPay — integrated payment processing accepting cards, PayWave, mobile payments, and e-wallets

Loyalty programme — "Treats" customer loyalty and marketing tools built in

Multi-outlet management — manage stock, pricing, and staff across branches from one dashboard

Offline capability — works without internet; transactions sync to the cloud on reconnection

Industry-specific modes — configured for retail, F&B, beauty, and service businesses

Pricing

Lite plan | Free (entry-level) |

Essential plan | S$56/month |

Hardware | Subscription model ("as low as $1/day") |

Transaction rates (QashierPay) | Not publicly published — contact Qashier |

Subscription options include annual, 2-year, and lifetime plans. A QSP (Qashier Support Package) sponsorship is available until 31 December 2026.

Pros & cons

Pros:

Free Lite plan available — lowest entry cost for a full POS in this list

Comprehensive feature set: inventory, loyalty, multi-outlet, and offline capability

Hardware via subscription — no large upfront purchase required

Industry-specific configurations for retail, F&B, beauty, and services

Cons:

Transaction rates not publicly published — requires direct contact

Hardware-dependent — more setup required than tap-to-phone solutions

More complex than merchants who only need card acceptance

Not suited to mobile, pop-up, or intermittent selling

Customers

Qashier suits established brick-and-mortar retailers who need inventory management, loyalty tools, and multi-outlet visibility. The free Lite plan may appeal to very early-stage retailers testing the waters. Businesses needing mobile or pop-up selling are better served by a tap-to-phone solution.

4. Stripe: Best for tech-forward omnichannel retailers

Stripe is a global payment platform with strong developer tools and a well-documented API. In Singapore, it offers Tap to Phone alongside its online payment infrastructure. That makes it a natural choice for retailers running both a physical shop and an online store.

Stripe is among the more expensive options for in-person Singapore card acceptance at 3.4% + $0.50. Its strength is breadth. Retailers with technical resources who sell across channels will find it one of the most capable platforms available.

It's worth noting that Stripe charges for PayNow, unlike using PayNow directly through your bank. For retailers who rely heavily on PayNow, that's an additional cost to factor in.

Key features

In-person Tap to Phone and online payment processing in one platform

Available on Android and iOS

Accepts Visa, Mastercard, and Amex

Transparent published pricing — no need to contact sales

Strong developer ecosystem and documentation

No setup fee, no monthly fee

Pricing

Card Type | Rate |

|---|---|

Singapore Visa / Mastercard | 3.4% + $0.50 |

Amex | 3.4% + $0.50 |

International Visa / Mastercard | 3.9% + $0.50 |

Additional 0.50% applies for international cards on top of domestic rates.

Pros & cons

Pros:

Online and in-person payments in one platform

Available on both Android and iOS

Transparent published pricing

Strong developer ecosystem for custom integrations

No setup fee, no monthly fee, no GST on fees

Cons:

Among the most expensive for in-person Singapore card acceptance (3.4% + $0.50)

Built primarily for online/e-commerce — Tap to Phone is an add-on

Charges for PayNow, unlike using it directly through a bank

Fixed pricing — no ability to negotiate rates

Better suited to technically capable teams than micro-retailers

Customers

Stripe's retail customers in Singapore tend to be tech-forward brands with an online presence. It's not the right fit for a micro-retailer who only sells in-person or who needs a simple, out-of-the-box setup.

5. NETS Tap-to-Phone: Best for traditional brick-and-mortar retailers

NETS is one of the longest-established payment networks in Singapore. Its Tap-to-Phone solution brings NETS acceptance to Android smartphones, including NETS debit card acceptance. This feature is not available on most competitors.

For traditional brick-and-mortar retailers with customers who pay by NETS debit, this is a meaningful differentiator. However, NETS comes with a monthly subscription fee of ~S$29.90 per device — regardless of how many transactions you process. For low-volume or seasonal retailers, that's a fixed cost that doesn't scale with your business.

The onboarding process is one of the most friction-heavy in the category. In 2026, NETS still requires a paper application form with a wet ink signature, mailed in. For retailers who need to get started quickly, this is a significant drawback.

Key features

NETS debit card acceptance — not available on most competitors

Tap-to-Phone on Android smartphones

Long-established brand widely accepted across Singapore retail

Pricing

Monthly fee | ~S$29.90 per device |

Transaction rate | Up to ~3.5% |

Setup | Paper application required (wet ink signature, mailed in) |

GST applies on fees. Monthly fee applies regardless of transaction volume.

Pros & cons

Pros:

Long-established, trusted brand in Singapore retail

NETS debit card acceptance — unique in the tap-to-phone category

Widely recognised and trusted by local consumers

Cons:

Monthly fee (~S$29.90/device) regardless of how much you sell

Paper application required — wet ink signature, mailed in — in 2026

Up to ~3.5% per transaction — among the most expensive rates in the category

Android only — no iOS support

Not suited for mobile, pop-up, or intermittent retail use

Customers

NETS Tap-to-Phone is best for established, higher-volume brick-and-mortar retailers where NETS debit acceptance is a genuine customer requirement and the monthly fee is justified by transaction volume.

6. Grab Tap to Phone: Best for merchants in the Grab ecosystem

Grab is primarily a super-app — ride-hailing, food delivery, financial services — with payment tools as a secondary offering. Its Tap to Phone solution offers competitive card rates and GrabPay acceptance at just 0.80%. This is particularly attractive for merchants whose customers are already in the Grab ecosystem.

The key caveat is GST. Grab adds 9% on all transaction fees, raising its 2.50% Singapore card rate to approximately 2.73% effective. Pricing is not publicly available — you'll need to reach a sales rep via WhatsApp.

Grab does not support Amex. For retailers serving international customers or higher-value transactions where Amex is common, this is a gap to consider.

Key features

GrabPay acceptance at 0.80% — highly competitive rate for the Grab ecosystem

Competitive Singapore Visa/Mastercard rates before GST

No setup fee, no monthly fee, no cancellation fees

Available on both Android and iOS

Pricing (before 9% GST)

Card Type | Rate |

|---|---|

Singapore Visa / Mastercard | 2.50% |

Amex | Not Supported |

International Visa / Mastercard | 3.20% |

GrabPay | 0.80% |

GrabPay / AliPay | 1.50% |

All rates subject to 9% GST. Pricing obtained via WhatsApp with Grab sales — not publicly published on the website.

Pros & cons

Pros:

Competitive base card rates (2.50% before GST)

GrabPay acceptance at 0.80% — best rate in category for GrabPay

No setup fee, no monthly fee, no cancellation fees

Strong consumer brand recognition in Singapore

Available on both Android and iOS

Cons:

9% GST on all fees — effective Singapore card rate is ~2.73%, not 2.50%

Does not support Amex

Pricing not publicly published — requires WhatsApp with sales

Grab is primarily a super-app; payment tools are not its core focus

Ecosystem advantage mainly benefits merchants serving Grab's consumer base

Customers

Grab Tap to Phone works best for F&B operators, retail merchants, and service providers whose customers are already active Grab users. The GrabPay rate of 0.80% is a genuine advantage in that context.

Frequently asked questions

What's the difference between a POS system and a card acceptance tool?

A full POS system includes inventory management, SKU tracking, and staff management — typically with dedicated hardware. A card acceptance tool focuses on payments only, with no inventory features. For small retailers with limited stock, the simpler approach is often cheaper and faster to get running.

Do I need a physical card terminal to accept payments in Singapore?

No. Solutions like nashi, HitPay, Stripe, and Grab let you accept contactless payments using an NFC-enabled smartphone. No card reader or terminal is required. The customer taps their card or wallet on your phone.

Which POS solution is cheapest for retail in Singapore?

For in-person card acceptance, nashi offers rates from 1.99% + $0.30 with no setup fee, monthly fee, or GST. NETS has among the highest per-transaction rates (up to 3.5%) plus a monthly fee. Stripe is among the more expensive on a per-transaction basis.

Is PayNow enough for my retail store?

PayNow is free to accept and great for local customers with Singapore bank accounts. But it doesn't work for tourists or international visitors. Card transactions also tend to be 30% higher in value — combining both gives you the best of both worlds.

Which options support Amex?

nashi, HitPay, and Stripe all support Amex. Revolut Business, Fiuu, NETS, and Grab do not.

How long does it take to start accepting payments?

nashi typically onboards merchants in 1 business day. HitPay and Stripe offer fast digital onboarding, though reviews note delays for some HitPay merchants. NETS has the slowest onboarding in the category — paper application, mailed in, taking significantly longer.

Conclusion: Which POS is right for your retail store?

The right choice depends on what your retail business actually needs. If you need a full POS with inventory management and hardware, Qashier is the strongest option. If you want an all-in-one platform covering in-person, PayNow, and online payments, HitPay is the most established local choice.

For small retailers and pop-up vendors who just need card acceptance, nashi is the most straightforward option. No hardware, no monthly fee, no GST on fees. Onboarding is typically completed in a single business day.

If GrabPay acceptance matters to your customers, Grab Tap to Phone offers a competitive rate. For traditional stores where NETS debit is a genuine requirement, NETS Tap-to-Phone remains the only option that covers it.